There is a ceiling of a credit card percentage, but banks ignore the principle and charge over 300% per year

{kind=link}

As part of the last year, Act No. 14.690 establishes that interest on a revolving loan on a credit card may not exceed 100% of the original debt value. This means that if the debt is 100 USD, the consumer cannot be charged within USD 200 to the end of 12 months.

Even with Act No. 14 690, which reduces the percentage of a speed loan on 100% of the original debt, banks still charge offensive fees, reaching over 300% per year. Lawyer João Carneiro suggests that in cases of inability to pay, the consumer does not pay off the debt to avoid consolidating the dirty name and look for future contracts or procudin help. TJMS offers default support via NUPEMEC, enabling an installment of up to 60 months. Debt priorities with a real warranty are recommended because they are more harmful than the dirty name that is reversible.

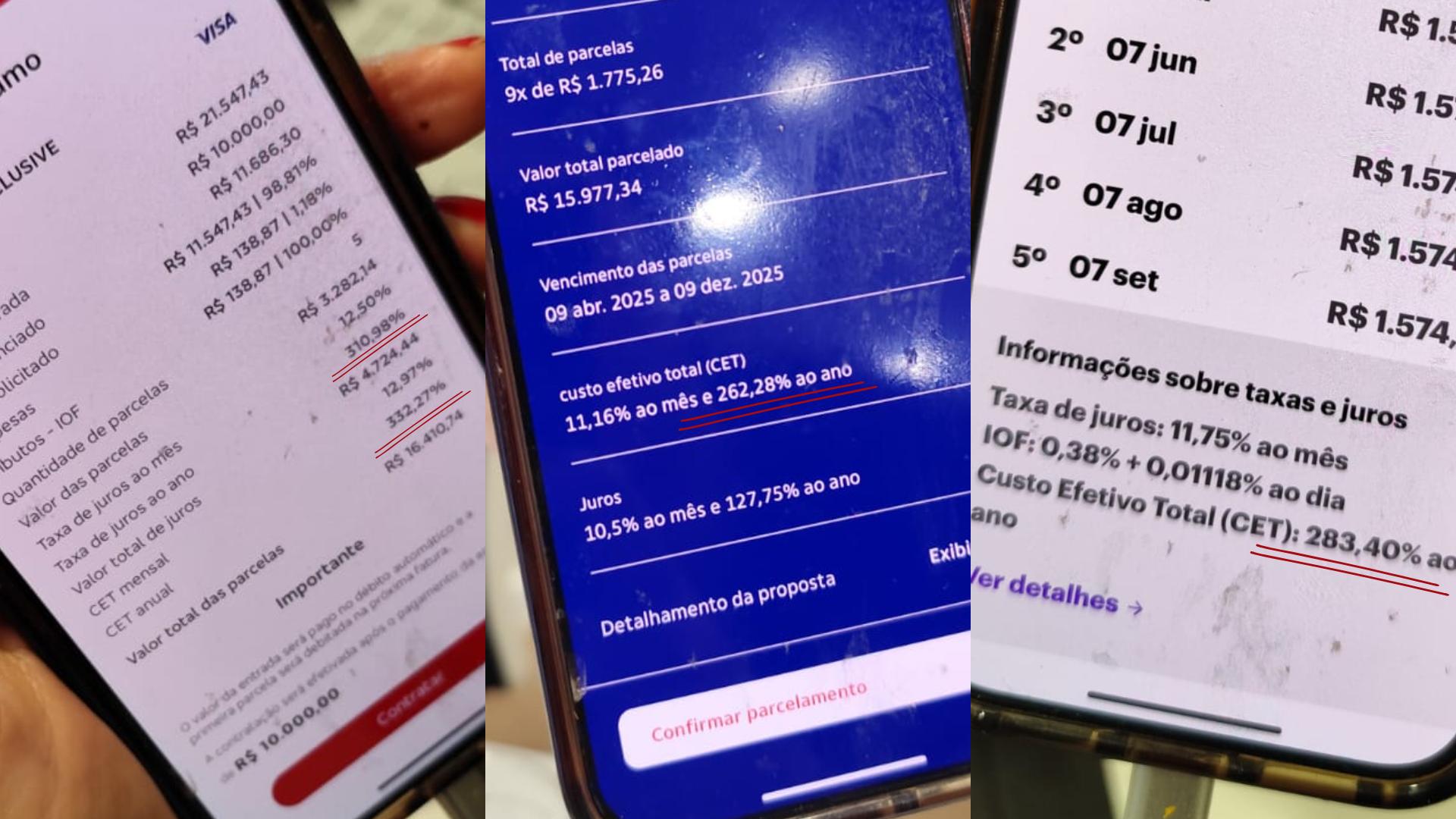

However, in practice, banks ignore the principle. Simulation made by Campo Grande News It shows that three leading financial institutions in the country are still charging interest much above the limit. Two traditional companies, with physical agencies, used annual rates of 332.27% (Bradesco) and 262.28% (Itú), while the popular virtual 283.40% (Nubank).

Thanks to this, in addition to dealing with the difficulty of repaying the original invoice amount, a consumer who decides to install the debt, it pays to take out the amount due.

Honest people hate themselves, but in the face of this scenario, temporary “default” is the only solution, the expert indicates. For lawyer João Carneiro, an expert in the field of consumer law, the answer may seem radical, but it is strategic: not pay.

“If you still recognize the debt, signing confession and renegotiation with interest of 300% per year, it will end the name Dirta forever. In everyday life I see that banks do not respect the rules. The consumer must protect themselves,” he says.

{kind=link}

John indicates that each case should be analyzed individually, but if the consumer is unable to pay and not act in bad faith, stop paying, it may be the only way. “Later, when the situation is improving, it is possible to try the contract. If you can’t, look for a percentage of your city or state,” he says.

Look for help – To meet the emergency renegotiation program, Brazil Mato Grosso for Sul Court of Justice (TJMS) has created a supporting sector for non -performance, Nupmec (a permanent center of conflict resolution methods).

According to Caroline Ascoli Freitas, advisers of special testicular projects, you can install debts within 60 months. “The law does not provide forgiveness, but the possibility of payments without a violation of the existential minimum. Discussions about interest or contractual clauses must be lodged to court, not to an earlier conciliation process,” he explains.

Despite the high interest rates on the card, João reassures: “This debt is not the most aggressive. Ideal is a priority long with a real guarantee, such as a car or property that violates immediate life. The dirty name is a problem, but it is reversible,” adds a lawyer.

Interested in negotiating, he should access the portal Court of Justice Mato Grosso to Sul. On the page you need to complete the form and attach the required documentation. Then Cejusc Over -insiteness is in contact to continue the process.

Services can also ask for channels: telephone (67) 3317-3997, e-mail survivement@tjms.jus.br or in person at one of the following addresses:

-

Cejusc Nupmec – Raul Pires Barbosa Street, 1.503, Chácara Cachoeira, Campo Grande;

-

Cejusc Commercial Association – November 15 Street, 390, Centro, Campo Grande.

Receive the main messages from what. Click here to access canal Campo Grande News And follow ours Social media.